Recent Articles

Your Equity Is Doing Nothing — Here’s How Smart Homeowners Use It

Find out about smart moves you can do with the equity built in your house.

Published on 04/01/2026

Smart Buyers Can Benefit When Rates Rise

Why High Rates Market Might Be a Smart Time to Buy

Published on 03/19/2026

Where an ARM (Adjustable-Rate Mortgage) May Be a Smarter Move

Find out when an ARM mortgage might be better than Fixed Rate Mortgage

Published on 03/05/2026

Is Refinancing Your Mortgage the Right Move?

Find out if refinancing is right for you.

Published on 02/27/2026

Housing Affordability in 2026: Why Rates Are not the Only Factor

Learn about home affordability factors with examples nationwide.

Published on 02/20/2026

Loyalty to Your Bank? Even With Your Home-Loan?

Decided whether you are should use your bank or a mortgage broker?

Published on 02/06/2026

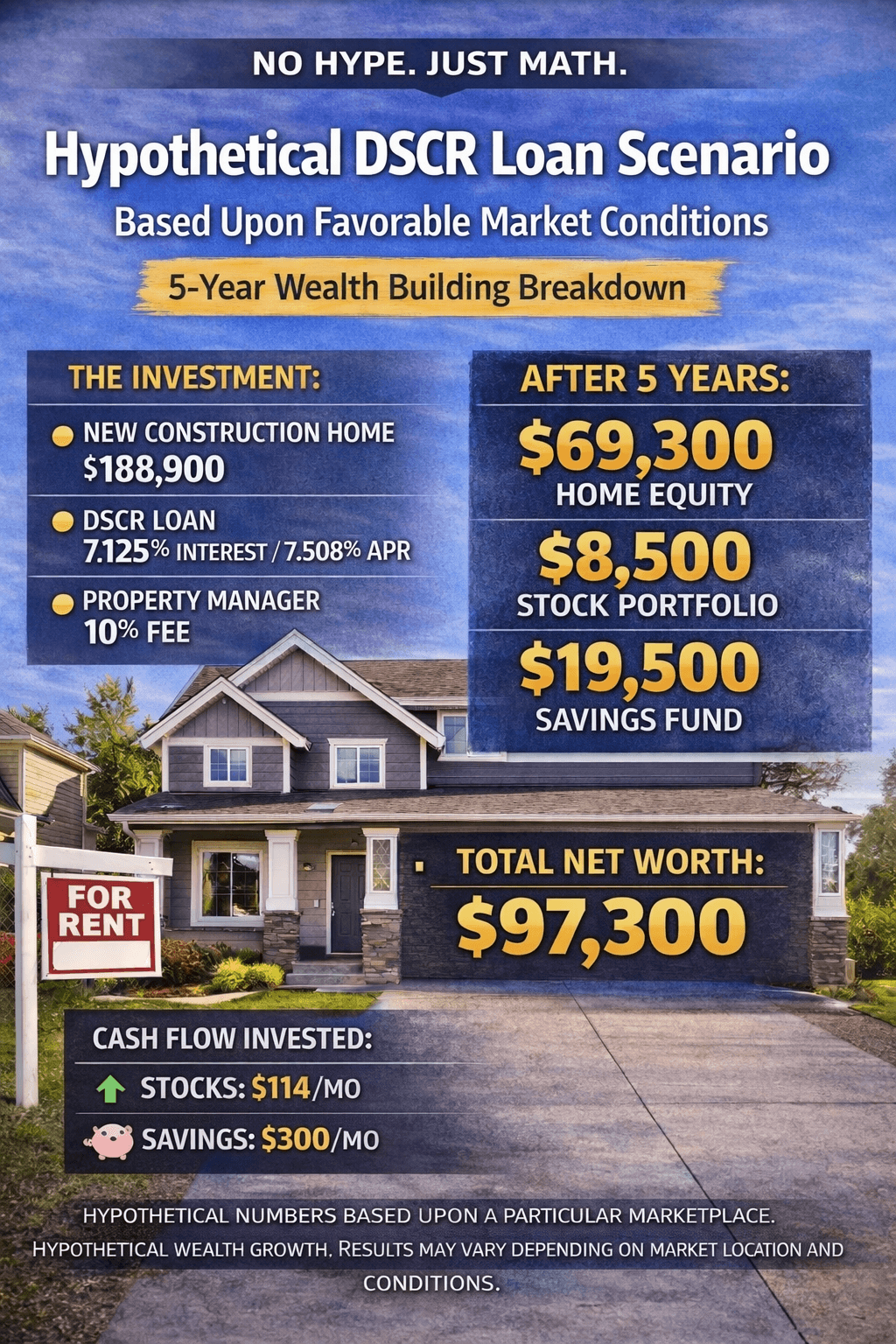

A Real-World DSCR Rental Scenario (5-Year Breakdown)

What the Numbers For A Hypothetical Real World DSCR Scenario Actually Looks Like With Property Management, Taxes, and Conservative Investing. Why This Scenario Matters: There’s no shortage of bold claims online about real estate investing — fast cash flow, early retirement, and “passive income” with no effort. This blog is different. What follows is a realistic DSCR rental scenario using: A modest brand-new home, Professional property management, Conservative rent increases, Modest appreciation, Disciplined investing of only the remaining cash flow, A high-income W-2 investor. No hype. Just math.

Published on 01/30/2026

Refinancing Isn’t Just About the Rate — It’s About Your Options

Learn what options refinancing makes available to you.

Published on 01/28/2026

How the NAR Lawsuit Changed Buyer Agent Compensation — and Why Professional Representation Still Matters

If you’re planning to buy a home, you may have heard that “commissions have changed” or that buyers are now having different conversations with real estate agents than they used to. Much of that confusion traces back to the Sitzer/Burnett v. NAR lawsuit and the industry-wide changes that followed. What this means for buyers today comes down to two critical realities: Buyer agent compensation is no longer assumed. Buyers should never assume the agent they are speaking with represents them. Both affect your money, your negotiating power, and even what information should remain confidential. Let’s break it all down clearly.

Published on 01/25/2026